Gazprom: Taxed into Loss by Russia To Pay For The War That Destroyed it’s Biggest Market

March 12 2026, before dawn. Ukrainian drones strike the Russkaya and Beregovaya compressor stations, the pumping

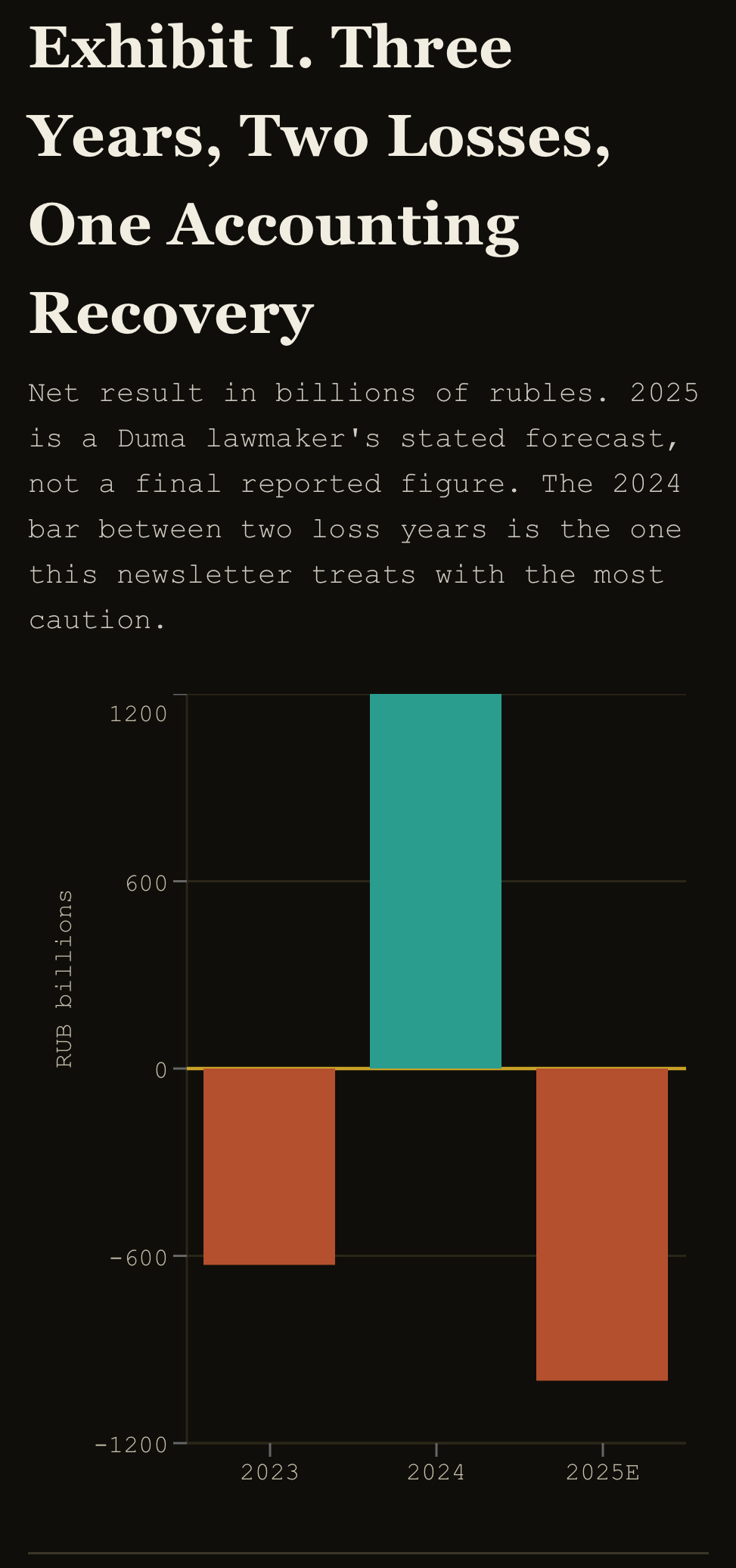

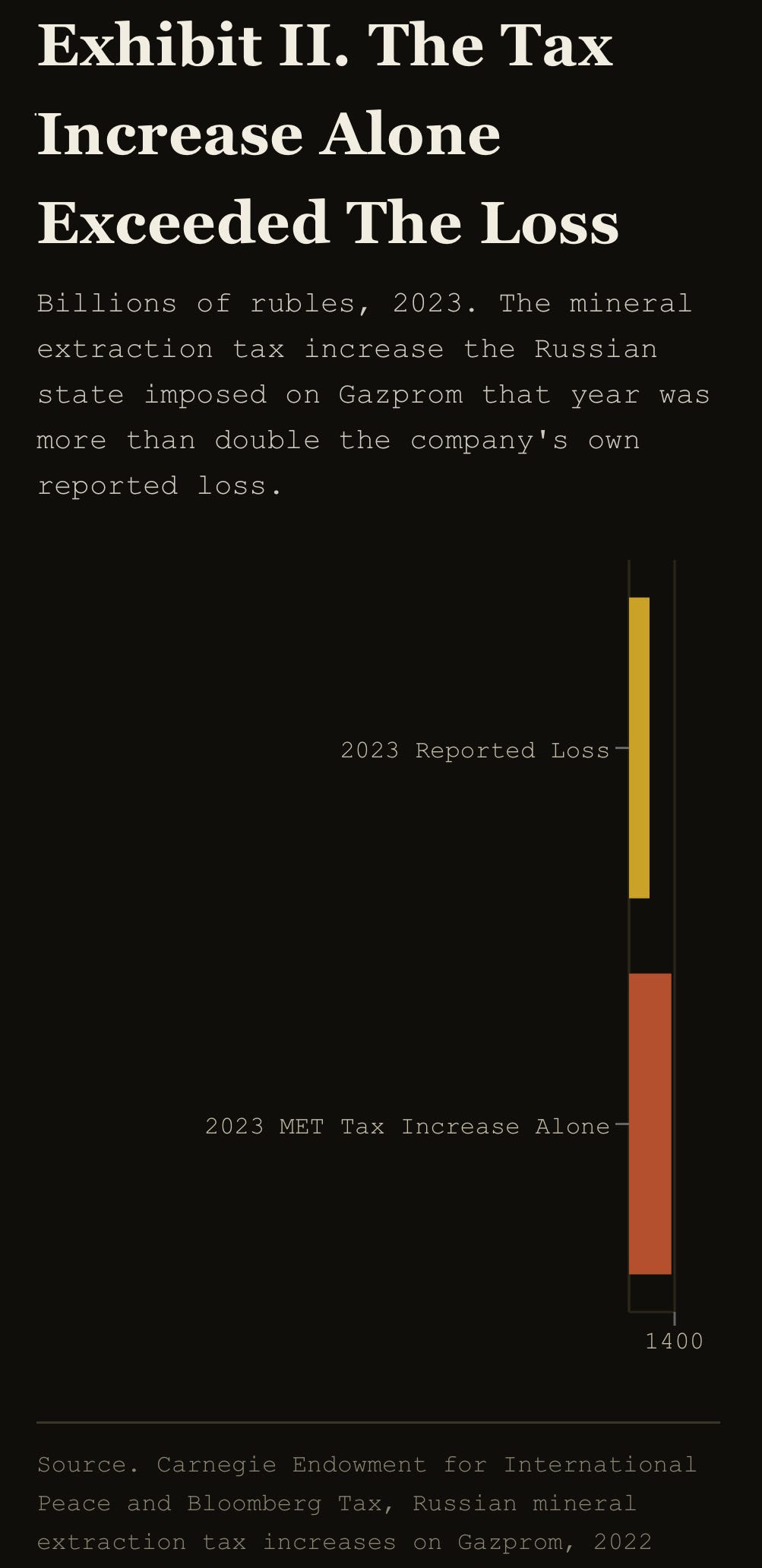

infrastructure feeding what remains of Gazprom’s export routes toward Turkey and southern Europe. It is not the first such strike and will not be the last. Three years earlier, in 2023, Gazprom posted a loss of six hundred twenty nine billion rubles, its first annual loss since 1999, a year before Vladimir Putin had even become prime minister. The war in Ukraine is the reason Gazprom lost its largest export market. The Russian state’s own tax code is the more immediate reason Gazprom actually lost money, since Moscow raised the mineral extraction tax on its own gas company specifically to fund the military spending that war required, costing Gazprom one point three trillion rubles in a single year, more than double the company’s headline loss. Gazprom did not simply lose the war’s collateral damage. It got taxed to help pay for the war directly.

THE LOSS, AND WHERE IT ACTUALLY CAME FROM

Strip away the tax increase and Gazprom’s underlying 2023 business looks considerably less catastrophic than the headline number suggests. Total revenue that year actually grew compared with pre war, pre pandemic 2019, from seven point six trillion rubles to eight point five trillion, despite losing most of the European gas market that had defined the company for decades. The real damage came from two sources layered on top of an already difficult year, the one point three trillion ruble mineral extraction tax increase Deputy Finance Minister Alexei Sazanov described plainly as an effort to skim windfall profits from oil and gas producers to fund the budget, and a separate one point one five trillion ruble writeoff of European assets, pipeline stakes, storage facilities, and joint ventures that had simply lost their value once the political relationship underpinning them collapsed, up from a mere twenty nine billion rubles in 2019.

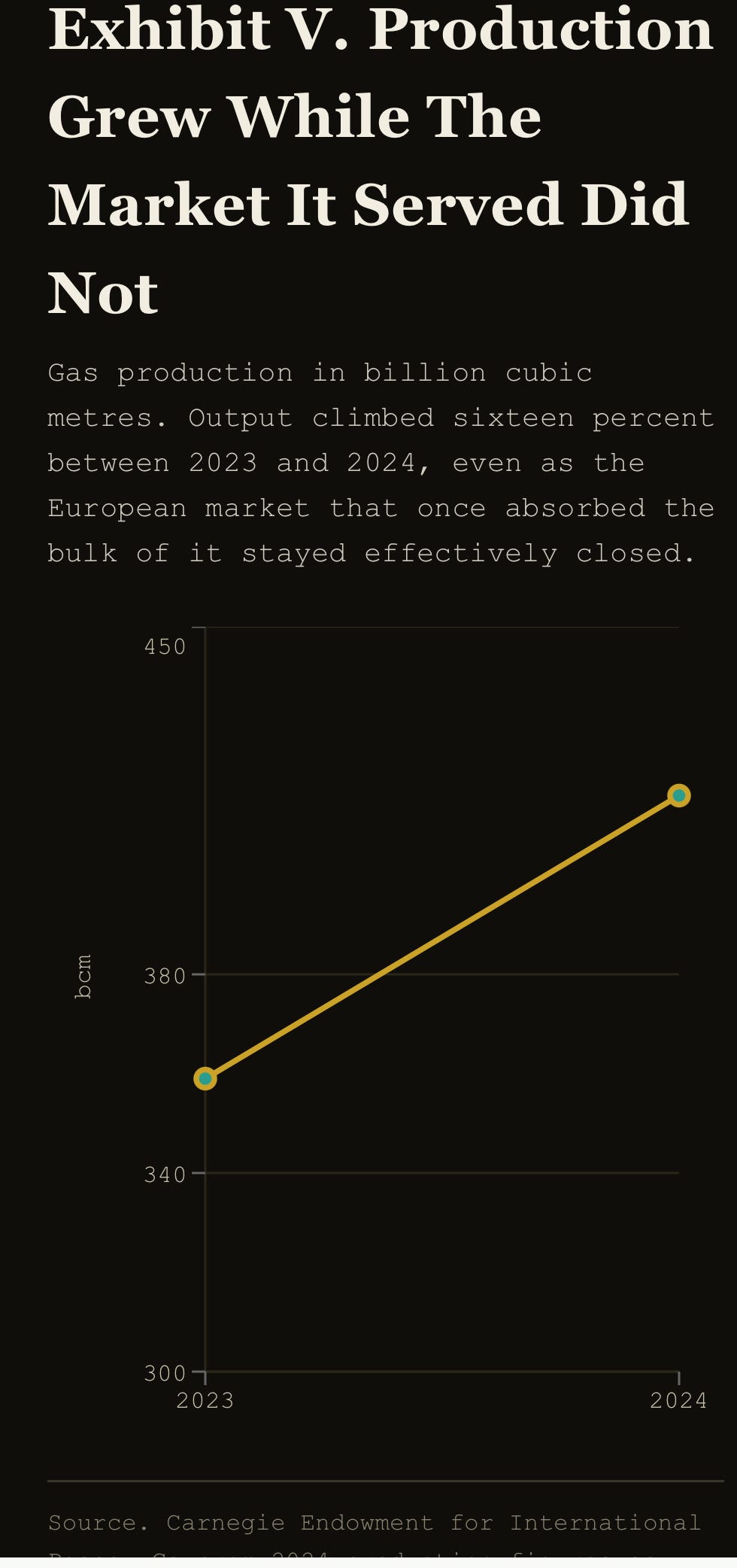

The following year produced a headline reversal striking enough to demand its own explanation. Gazprom’s 2024 IFRS results showed a net profit of one point two trillion rubles, and the mechanics behind that swing say more about accounting opportunism than operational recovery. Gazprom paid ninety four billion rubles for Shell’s twenty seven point five percent stake in Sakhalin Energy, the operator of the Sakhalin Two liquefied natural gas project, in March 2024, yet recognized an immediate accounting gain of roughly a hundred ninety one billion rubles because the purchase price sat well below the asset’s fair value following Shell’s forced exit, a paper gain rather than cash in hand, but one IFRS rules required Gazprom to book in full the moment the deal closed. Shell itself wrote off one point six billion dollars walking away from the same stake. One company’s forced retreat became another company’s accounting windfall, and the full consolidation of Sakhalin Energy’s revenue from the second quarter of 2024 onward added four hundred sixty four billion rubles to Gazprom’s books entirely on its own. Layer in another trillion rubles from oil, gas condensate, and refined product sales, boosted by a Urals crude price running six dollars a barrel higher than the year before on essentially flat physical volumes, and the picture of 2024’s turnaround becomes clear, a company that grew gas production from three hundred fifty nine billion cubic metres to four hundred sixteen billion, but whose profit swing depended just as heavily on one opportunistic acquisition and a favorable oil price as it did on any structural repair of the European market it had actually lost.

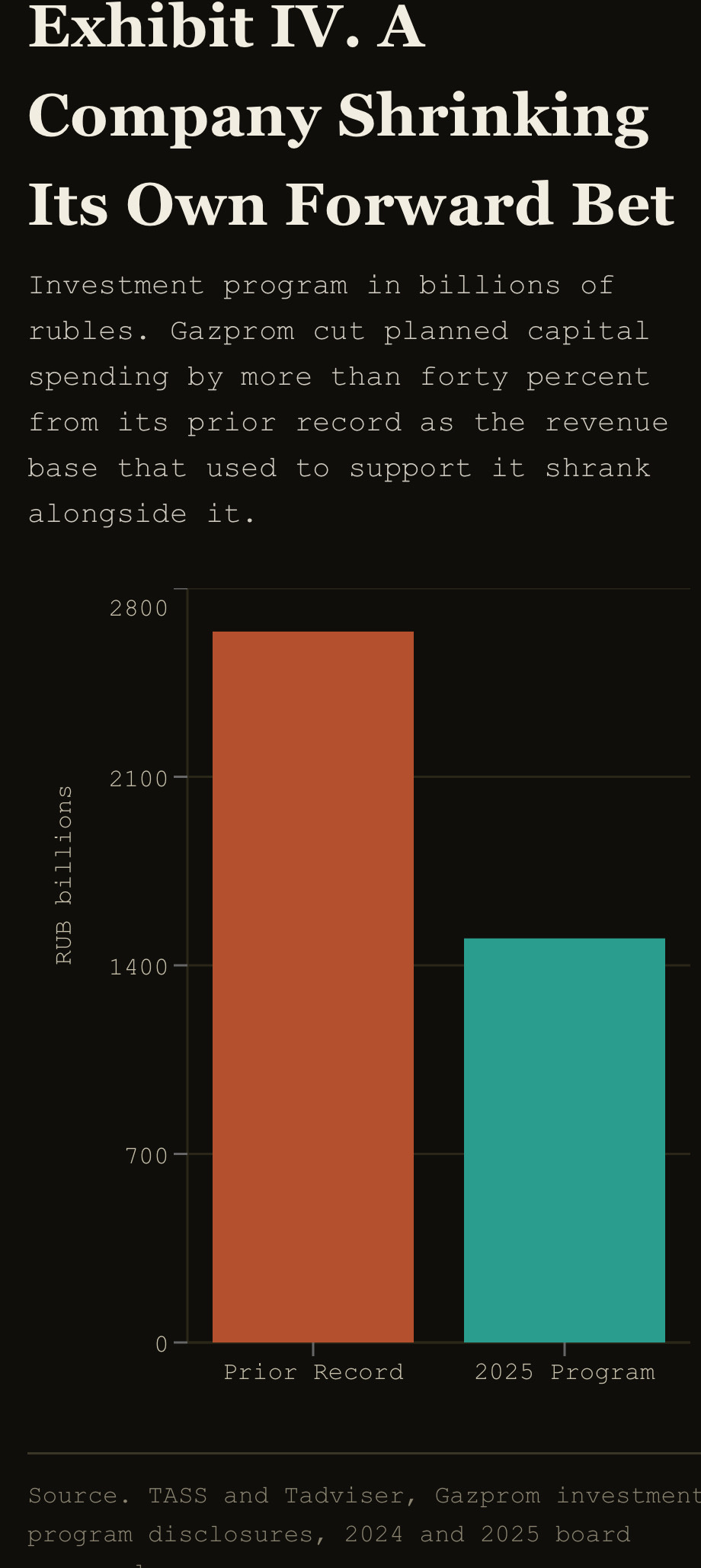

That repair still has not happened, and 2025 showed the tax pressure has not eased either. A Duma lawmaker warned in committee that Gazprom’s continued tax burden, layered onto declining export revenue, could drive the company to another loss approaching a trillion rubles for the year, telling colleagues that gas transportation costs keep rising even as the export volumes that once justified that infrastructure keep falling. Gazprom’s own board cut the 2025 investment program to one point five trillion rubles, down from a record above two point six trillion in prior years, a company deliberately shrinking its own forward capital commitment because the revenue base that used to support a larger one no longer exists.

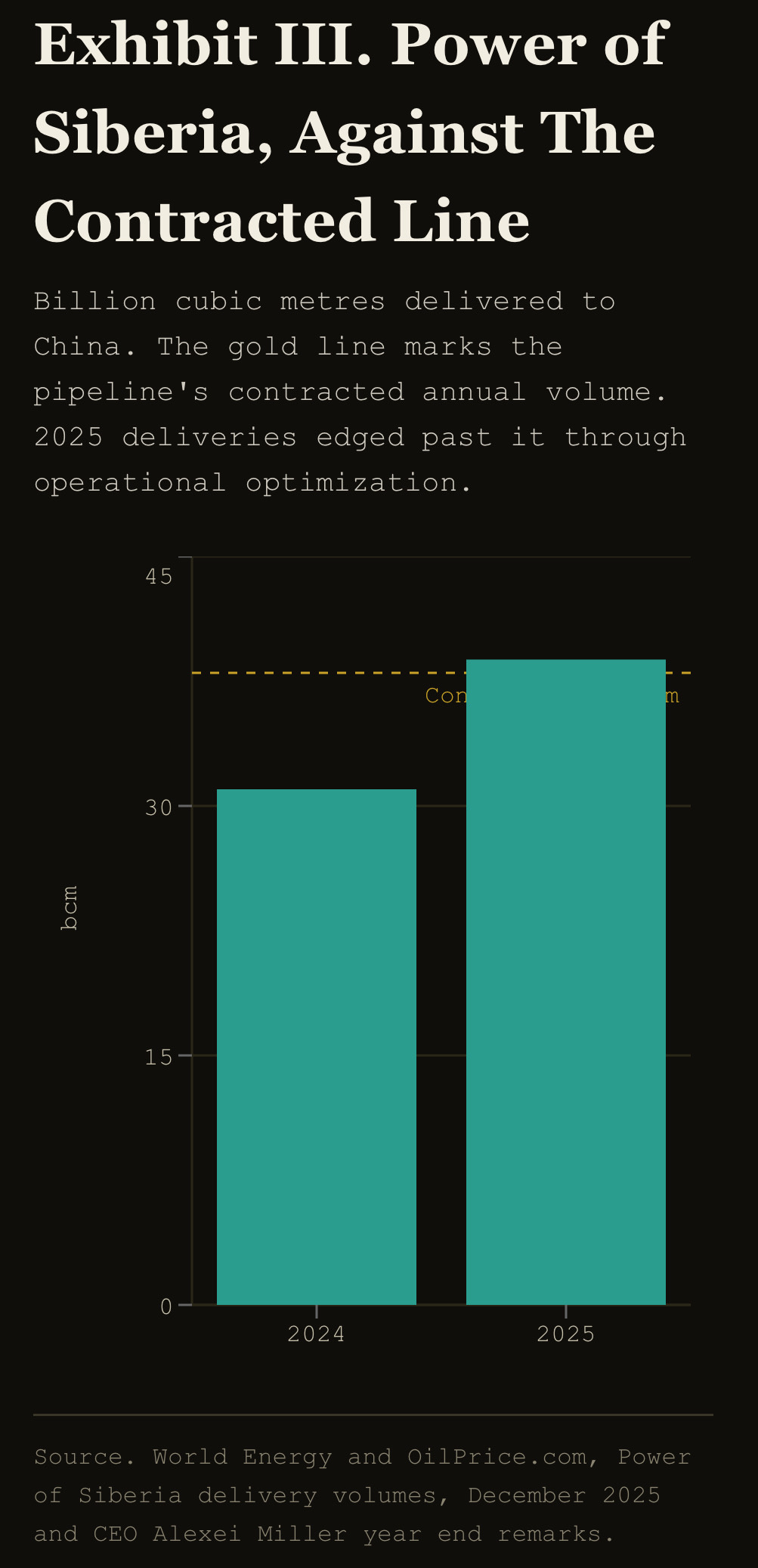

THE PIVOT TO CHINA, MEASURED AGAINST WHAT IT REPLACED

Gazprom’s answer to losing Europe has been the Power of Siberia pipeline into China, and 2025’s results show real progress against a genuinely small base. Deliveries reached thirty eight point eight billion cubic metres for the year, nearly twenty percent above 2024’s thirty one billion, slightly exceeding the pipeline’s contracted annual volume of thirty eight billion cubic metres through operational optimization, with chief executive Alexei Miller telling reviewers Gazprom delivered almost eight hundred million cubic metres beyond its contractual obligation to China. That is a genuine operational achievement. It is also a fraction of what Gazprom used to sell into Europe at the relationship’s peak, when annual pipeline exports ran several multiples higher than the volume China currently takes, meaning the pivot east has replaced a portion of the lost market rather than the whole of it, years into the effort.

The next leg of that pivot, Power of Siberia Two, running through Mongolia, remains stuck in negotiation despite years of intergovernmental agreements and memoranda between Moscow and Beijing. Neither side has signed a final investment decision or a binding gas purchase contract, and the sticking point is the same one that stalls most deals between a desperate seller and a buyer with no urgency, price, with China reportedly unwilling to commit to terms anywhere near what Gazprom needs to justify the pipeline’s cost. Construction could take up to a decade even once terms are settled, according to estimates from China’s own state energy officials, and financing for a project this size remains unresolved. Turkey has, in the meantime, quietly become Russia’s largest remaining market touching Europe at all, surpassing the European Union itself as a destination for gas moving through the TurkStream system, the same infrastructure the March 2026 drone strikes targeted directly.

Worth noting plainly, Gazprom itself is barely a participant in Russia’s other major gas growth story, liquefied natural gas. Novatek, not Gazprom, is Russia’s dominant LNG exporter, running the Yamal LNG project under a twelve year exemption from the same mineral extraction taxes that have been squeezing Gazprom specifically, an asymmetry in how Moscow treats its two gas companies that itself says something about which one the state currently needs more from and which one it is willing to let keep more of its own revenue.

THE POLITICS OF A COMPANY THE STATE NEEDS TO BLEED

Gazprom’s relationship with its own government is not adversarial in the way sanctions politics is adversarial. It is closer to a landlord extracting rent from a tenant it also happens to own outright. The mineral extraction tax increases that drove the 2023 loss were not imposed by a hostile foreign power, they were imposed by the Russian Ministry of Finance, explicitly to help fund the same war effort that had already cost Gazprom its largest export market in the first place, a closed loop in which the company simultaneously supplies the state’s energy leverage abroad and gets taxed at home to underwrite the conflict that leverage is being used to fight. Deputy Finance Minister Sazanov’s own language, skimming windfall profits, treats Gazprom’s revenue as a national resource to be drawn down whenever the budget requires it, regardless of what that draw down does to the company’s own reported financial health.

The March 2026 strikes on Russkaya and Beregovaya sit inside a broader pattern of Ukrainian attacks specifically targeting the compression infrastructure that keeps gas moving toward whatever export markets remain, a campaign that treats Gazprom’s remaining pipeline capacity as a legitimate military target precisely because that capacity still generates hard currency and diplomatic leverage for Moscow. Purely as speculation rather than anything settled, Kirill Dmitriev, representing Russia’s sovereign wealth fund in periodic contact with American counterparts, has continued raising the possibility of restoring elements of the energy relationship between Washington and Moscow. Whether that speculation ever touches Gazprom specifically remains unclear, and the connection between Dmitriev’s public comments and Gazprom’s own future is not one the available evidence currently supports beyond noting that any broader resolution to the war would likely affect the company eventually.

WHAT THE TAPE IS SAYING NOW

Europe’s own diversification away from Russian gas, accelerated LNG imports from the United States and Qatar, expanded storage capacity, demand destruction from higher prices sustained since 2022, has done to Gazprom’s addressable market roughly what a determined new entrant does to an incumbent anywhere else, permanently shrinking the base the incumbent can ever fully recover, regardless of how the underlying war eventually resolves. China exports deflation into whatever industry it decides to scale, and the global LNG market is scaling hard through the back half of this decade, Qatar’s North Field expansion, the American Gulf coast build out, Mozambique’s eventual capacity, all arriving inside the same window Gazprom is trying to negotiate Power of Siberia Two into existence. Gazprom is not just negotiating against Chinese price resistance. It is negotiating against a global gas supply picture that gives Beijing less reason every year to accept Moscow’s price rather than wait for cheaper alternatives to reach the market instead.

STRESS TEST

China’s negotiating leverage over Power of Siberia Two is overwhelming rather than absolute, since Gazprom has far fewer alternative buyers than China has alternative suppliers, a dynamic that will keep pricing negotiations stalled for as long as China calculates that waiting costs it nothing.

Infrastructure risk is now a permanent operating condition rather than an occasional disruption. Compressor stations feeding Gazprom’s remaining export routes sit inside active strike range for the duration of the war, and every ruble spent on repair is a ruble unavailable for the capital program the company has already been forced to shrink twice.

Fiscal extraction risk never actually goes away once a government has demonstrated it will raise taxes on a state company whenever the budget needs it. The 2023 precedent means any future revenue recovery Gazprom manages to generate is immediately vulnerable to the same mechanism that produced the 2023 loss in the first place.

THE INSTITUTIONAL LABEL

Gazprom subsidizes. The company has moved through three distinct identities without ever changing its name. In the 1990s it operated as a commercial gas monopoly, Russia’s answer to what a state owned utility could become once the Soviet system dissolved around it. Through the 2000s and into the 2010s it became a geopolitical instrument, selling gas to Europe on terms that doubled as leverage over the continent’s own energy security, a role that made Gazprom as much a foreign policy tool as an energy company. In the 2020s it became something narrower and more transactional, a fiscal instrument financing the Russian state budget directly, taxed at a rate calibrated to whatever the war currently costs, treated by its own government as a reserve to be drawn down rather than a business to be protected. Rosneft absorbed sanctions imposed from outside the country. Gazprom absorbed a tax increase imposed from inside it, for the same underlying reason, and the distinction matters, because a foreign sanctions regime can theoretically be negotiated away in a peace settlement. A domestic tax precedent, once set, belongs to Moscow to reimpose whenever it likes, war or no war, for as long as Gazprom remains too strategically important for the state to ever fully let go of.

SOURCES

Sergey Tereshkin Publications, Gazprom RAS first half 2025 results analysis. Carnegie Endowment for International Peace, how Gazprom went from record losses to profits, coverage of 2023 and 2024 IFRS results. World Energy and OilPrice.com, Power of Siberia 2025 delivery volumes and Power of Siberia Two negotiation status, December 2025. TASS, Duma Committee on Budget and Taxes coverage of Gazprom’s 2025 loss forecast and mineral extraction tax increases, including reporting on the March 2026 Russkaya and Beregovaya compressor station strikes. Atlantic Council, effect of sanctions and windfall taxation on the Russian energy industry, including the Novatek mineral extraction tax exemption comparison. Bloomberg Tax, Russia’s 2022 proposed mineral extraction tax increases on Gazprom.