TotalEnergies: A Billion Dollars To Stop By The Same Government That Sold It The Right To Start

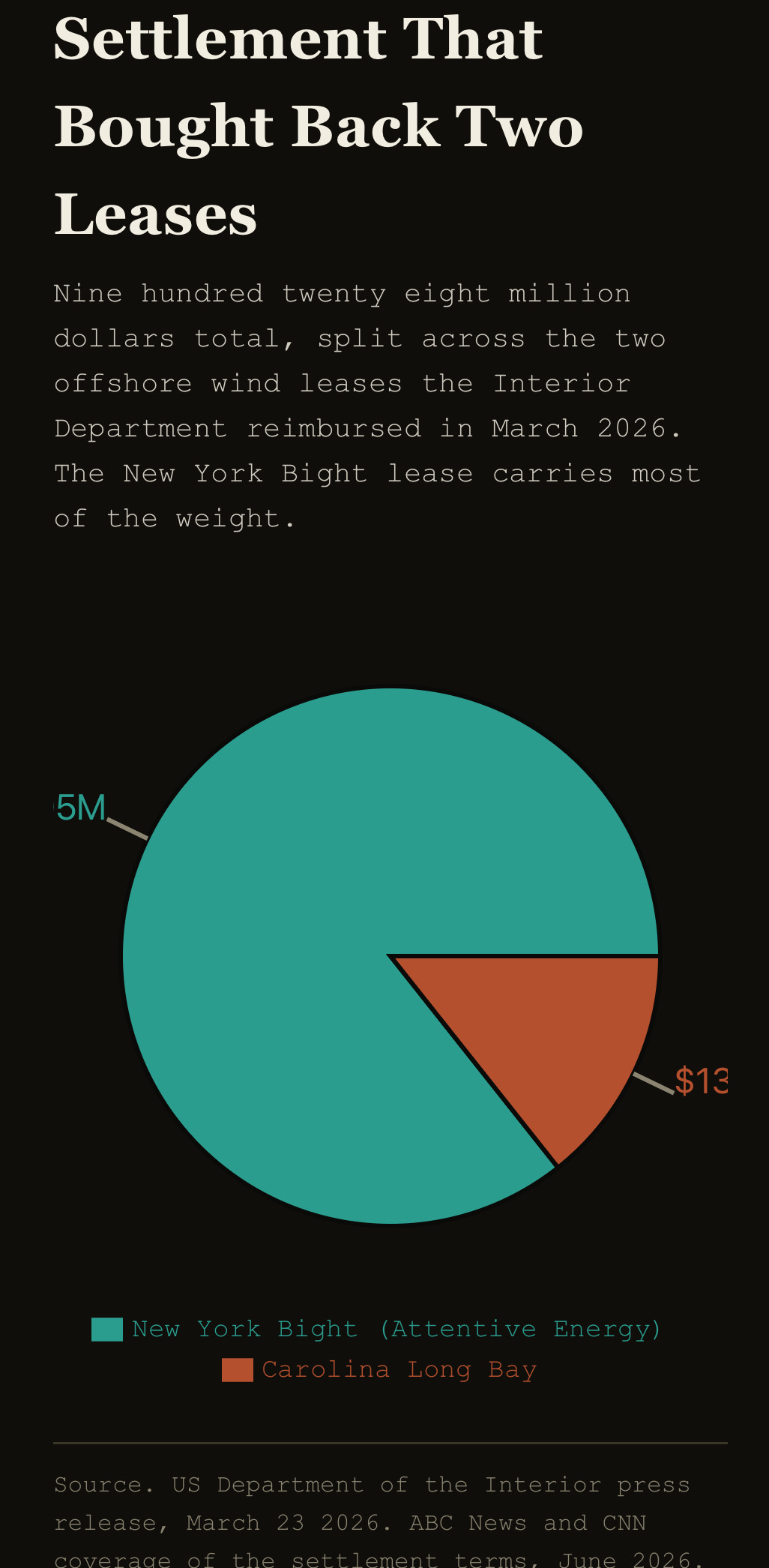

Houston, March 23 2026, CERAWeek. Patrick Pouyanne stands next to Interior Secretary Doug Burgum and signs away two offshore wind leases his own company bought in 2022 for a combined nine hundred twenty eight million dollars. Washington hands the money straight back, up to what TotalEnergies originally paid, and Pouyanne pledges to steer the refund into American gas projects including Rio Grande LNG. Told there might be more deals like this one coming, Pouyanne says maybe TotalEnergies opened the door first. Seven state attorneys general call the whole arrangement a sham three months later and drag it into federal court.

Sit with the shape of that trade for a second. A French company bought American seabed rights from one administration, held them for four years, then walked away from a settlement that reimbursed the company for what it originally paid, funded through the federal Judgment Fund, with a pledge attached to redeploy the cash into gas. Nobody forced TotalEnergies into anything. The company simply read which way Washington’s money was now flowing and pointed its sails there, exactly the same instinct that has kept this company alive through nationalization in Iran, war in Libya, sanctions in Russia, insurgency in Mozambique, and a court in Paris that has been trying to pin it down on Uganda since 2019. TotalEnergies does not pick a side. It reads the weather and adjusts the rigging, every single time, and 2025 was the year that skill got tested on four continents at once.

THE NUMBERS BUILT LAYER BY LAYER

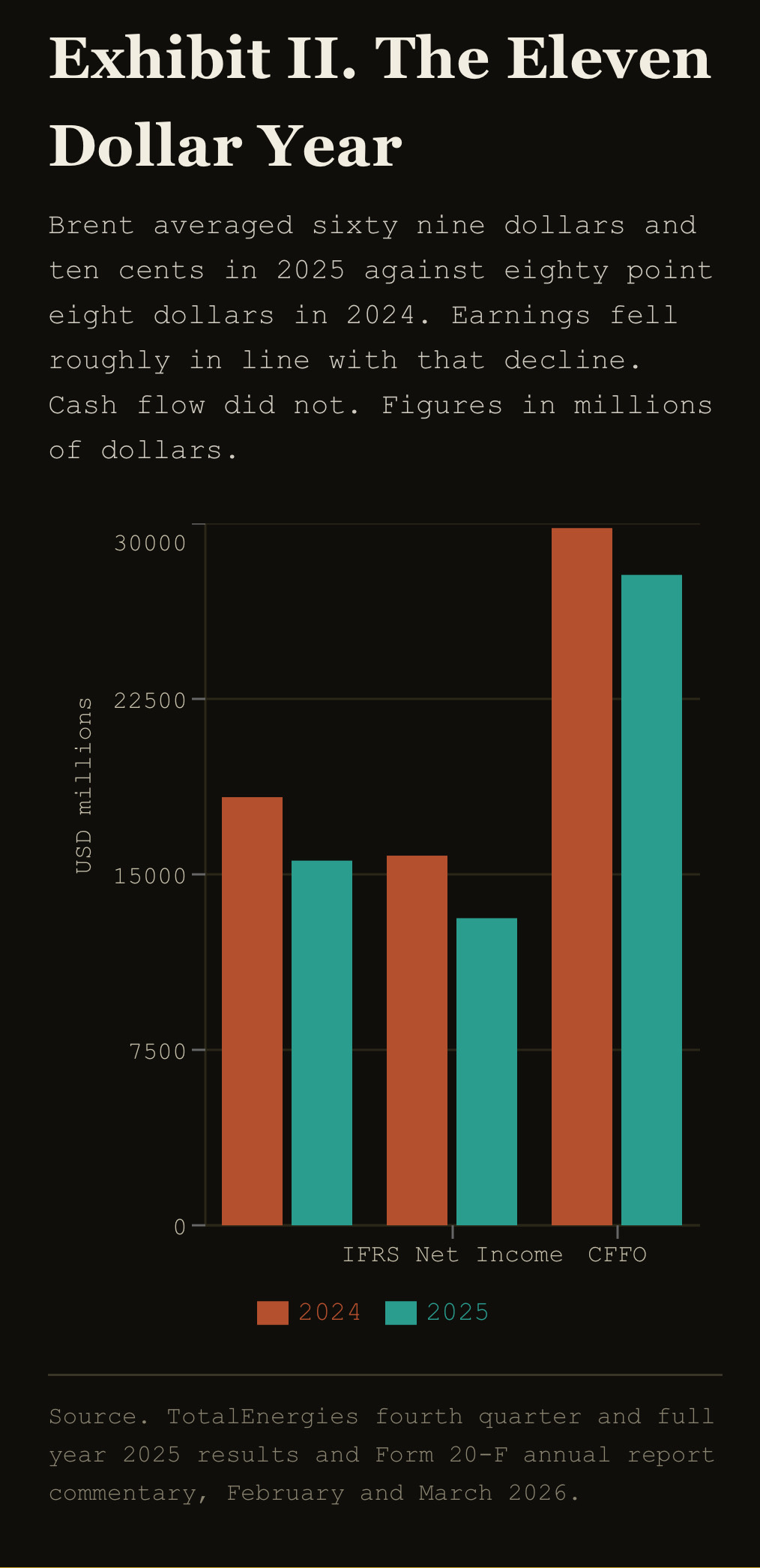

Brent averaged sixty nine dollars and ten cents a barrel in 2025, down from eighty point eight dollars in 2024, an eleven dollar drop that would have gutted a pure producer. TotalEnergies absorbed five dollars of that eleven dollar decline through production growth alone and still finished the year with adjusted net income of fifteen point six billion dollars, down fifteen percent, and reported net income of thirteen point one billion dollars, down seventeen percent. Cash flow from operations fell only seven percent to twenty seven point eight billion dollars, the gap between the fifteen percent earnings decline and the seven percent cash decline being the entire argument for owning an integrated major instead of a pure upstream one. Return on average capital employed held at twelve point six percent, the best among the five western majors for a fourth consecutive year running.

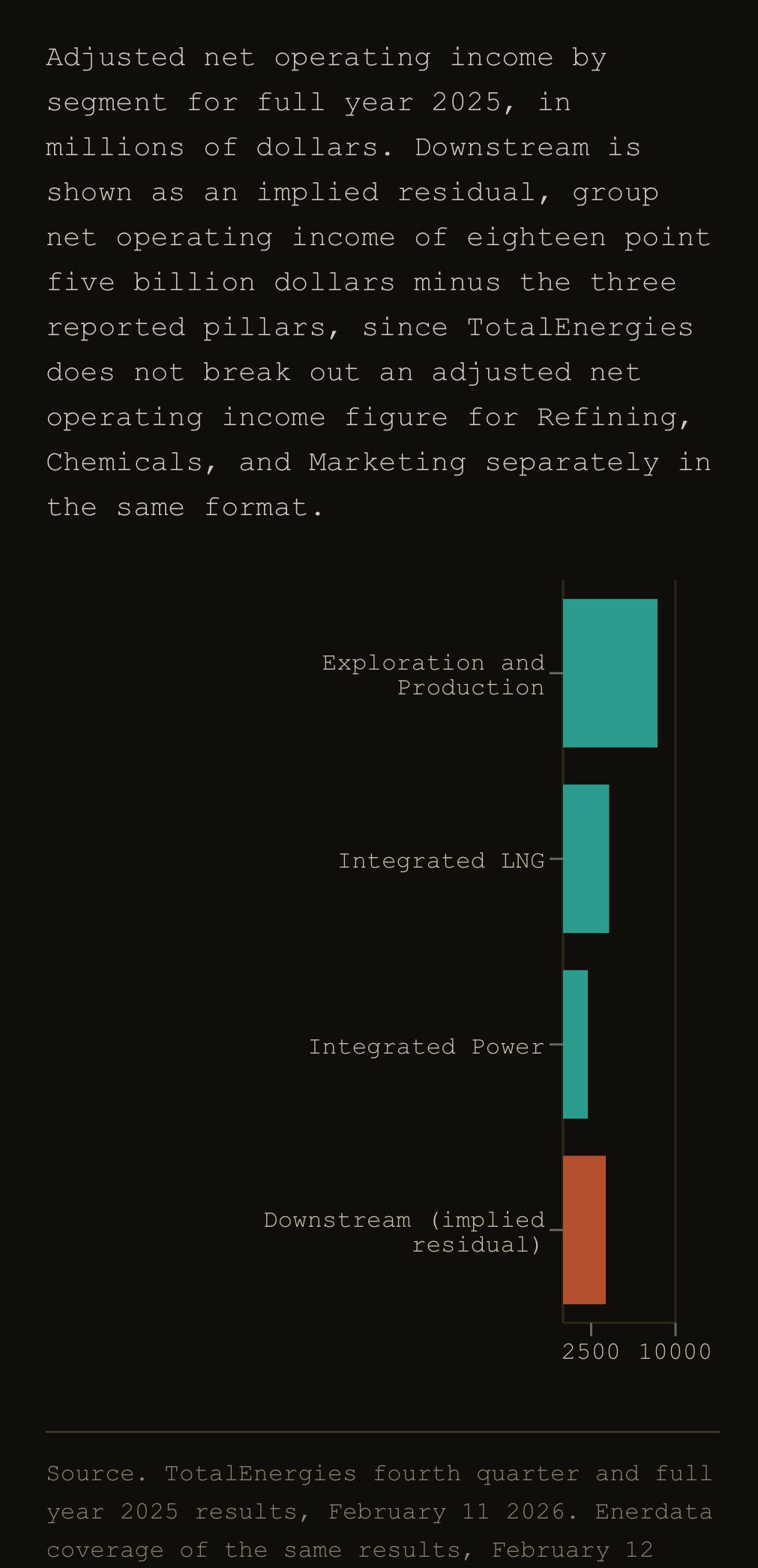

Exploration and Production delivered adjusted net operating income of eight point four billion dollars and cash flow of fifteen point six billion, with hydrocarbon output climbing nearly four percent to two thousand five hundred twenty nine thousand barrels of oil equivalent a day. Seven major projects started or continued their ramp through the year, Mero three and Mero four in Brazil advancing alongside the already running Mero two, plus Anchor and Ballymore in the American Gulf, Fenix in Argentina, and Tyra in Denmark, and reserve replacement came in at a hundred sixteen percent, meaning the company found more oil and gas than it produced across the year. Integrated LNG added four point one billion dollars of adjusted net operating income and four point seven billion of cash flow, on sales of forty three point nine million tonnes, up ten percent. Integrated Power, the newest and most experimental pillar, generated two point two billion dollars of adjusted net operating income and two point six billion of cash flow on a return on capital employed of ten percent, net electricity production climbing seventeen percent to forty eight point one terawatt hours across thirty four point one gigawatts of installed renewable capacity.

Four pillars, one balance sheet. Gearing rose to fourteen point seven percent from eight point three percent the year before and five percent the year before that, net debt climbing to twenty point two billion dollars. The dividend rose to three euros forty per share, up five point six percent, alongside seven point five billion dollars of buybacks. This is a company spending more than it earns in cash returns during a year its earnings fell by double digits, a bet that 2025 was the trough rather than the new normal.

MOZAMBIQUE, BACK FROM THE DEAD

January 29 2026, Afungi, Cabo Delgado province. Pouyanne stands with Mozambican President Daniel Chapo and announces the full restart of Mozambique LNG, a twenty billion dollar project frozen since 2021 when an insurgent assault near the site, with trade press coverage at the time placing the death toll near eight hundred, forced every foreign worker off the peninsula. The consortium lifted its force majeure declaration on November 7 2025 after four years of security work alongside Rwandan forces, and by the January announcement more than four thousand workers were mobilized on site, over three thousand of them Mozambican. TotalEnergies is not alone in this. Mozambique’s own state hydrocarbons company, Mitsui, PTTEP of Thailand, and two Indian state companies, ONGC Videsh and Oil India, all hold pieces of the project, meaning an ONGC subsidiary has capital sitting in the same ground TotalEnergies just declared safe enough to rebuild on. First gas is targeted for 2029, the project sitting at roughly forty percent complete, with around four to four and a half billion dollars already spent across the pause years on site upkeep, engineering, and procurement that continued even while construction itself stood still.

Rebuilding does not erase what happened in 2021. TotalEnergies is currently facing two separate legal proceedings in France tied to that year. A manslaughter investigation examines whether the company failed to protect subcontractors during the Palma attack. Separately, a German human rights group filed a complaint with France’s counterterrorism prosecutor alleging complicity in war crimes, torture, and enforced disappearance, built on claims that TotalEnergies financed and materially supported the Mozambican military task force accused of detaining, torturing, and killing dozens of people in the months after the attack. Both cases remain open while the company pours another fifteen billion dollars of remaining capital into the same ground.

UGANDA, THE CASE THAT WILL NOT CLOSE

TotalEnergies holds sixty two percent of the East African Crude Oil Pipeline, a heated line running roughly fourteen hundred kilometers from Uganda’s Lake Albert fields to the Tanzanian coast, feeding off the Tilenga development that drills four hundred nineteen wells, a third of them inside Murchison Falls National Park. French NGOs first sued the company in October 2019 under France’s duty of vigilance law, a 2017 statute requiring large French companies to actively prevent human rights and environmental harm across their operations. That first case died on procedure in 2023. A second and tougher case followed in June 2023, filed by twenty six directly affected Ugandans alongside five French and Ugandan organizations, seeking actual reparations rather than a project suspension. On September 18 2025 the Paris court ordered TotalEnergies to hand over internal audits, compensation calculations, and Human Rights Steering Committee minutes the plaintiffs had been chasing for nearly two years, ruling that the parent company could not hide behind its subsidiaries to avoid disclosure. A hearing on the actual merits is expected sometime in 2026. NGOs claim more than a hundred thousand people across Uganda and Tanzania have lost full or partial use of their land to the two projects. TotalEnergies maintains its vigilance plan meets every requirement the 2017 law sets out and that no fault has been established.

THE POLITICS OF THREE CAPITALS

Washington wrote the biggest political story of TotalEnergies’ year. The wind lease buyback sits inside a wider Trump administration campaign against offshore wind that includes withdrawing the Outer Continental Shelf from future wind leasing and canceling hundreds of millions in federal funding for other projects, and internal Interior Department documents later showed TotalEnergies did not actually need to make any new investment to collect its refund, since it could simply submit receipts for oil and gas spending already underway. Interior Secretary Burgum told Congress the company was merely refunded money it had already redeployed, calling it an interest free loan the government returned. New York Attorney General Letitia James, leading six other states into court, argued the deal broke federal procedure by skipping a legally required hearing on national security harm and violated the statute governing the Judgment Fund the payment came from. TotalEnergies has not had to answer publicly for any of it, since the lawsuit targets the federal government, not the company that walked away with the check.

Paris tells a quieter but equally political story. Nearly half of TotalEnergies’ institutional shareholders now sit in the United States, up from a third in 2012, while the French share of ownership has shrunk to under a fifth. Rather than force the fight Bruno Le Maire once promised to wage against a full New York relocation, the company found the middle path in September 2025, when its board approved converting the ADRs it had carried on the New York Stock Exchange since 1991 into ordinary shares trading directly in New York, completed that December, while formally keeping Paris as the company’s home listing and headquarters. France gets to keep the flag. America gets the liquidity. Nobody in Paris had to lose a public fight to get there, which may be the most French outcome available.

Maputo and Kampala are the capitals TotalEnergies actually needs something from rather than the other way around. Chapo’s government confirmed continued security cooperation with Rwanda as the price of restarting Mozambique LNG, an arrangement that keeps foreign troops on Mozambican soil indefinitely in exchange for the jobs and tax revenue a functioning gas export terminal would bring. Uganda’s government under Yoweri Museveni pushed EACOP through parliamentary approval years ago over opposition objections about inadequate compensation, and continues defending the project publicly while TotalEnergies fights the same allegations in a French courtroom four thousand miles away. In both countries the calculation is identical. A struggling government needs the revenue more than it needs the fight, and TotalEnergies is patient enough to wait out whichever side blinks first, in Paris, in Washington, or in the capital actually sitting on the resource.

WHAT THE TAPE IS SAYING NOW

TotalEnergies built its 2026 guidance on sixty dollar Brent, a full nine dollars below the 2025 average and a hundred dollars below where the war briefly pushed prices in April. Amrita Sen of Energy Aspects told CNBC’s Squawk Box in late June that the market still underestimates how far shipping conditions in the Gulf remain from a genuine pre war normal, tankers still avoiding routes they used freely before February. Around the same week, Kevin Hassett framed the current calm as a ledge rather than a landing, arguing a coming wave of new supply will push prices lower once shipping fully normalizes.

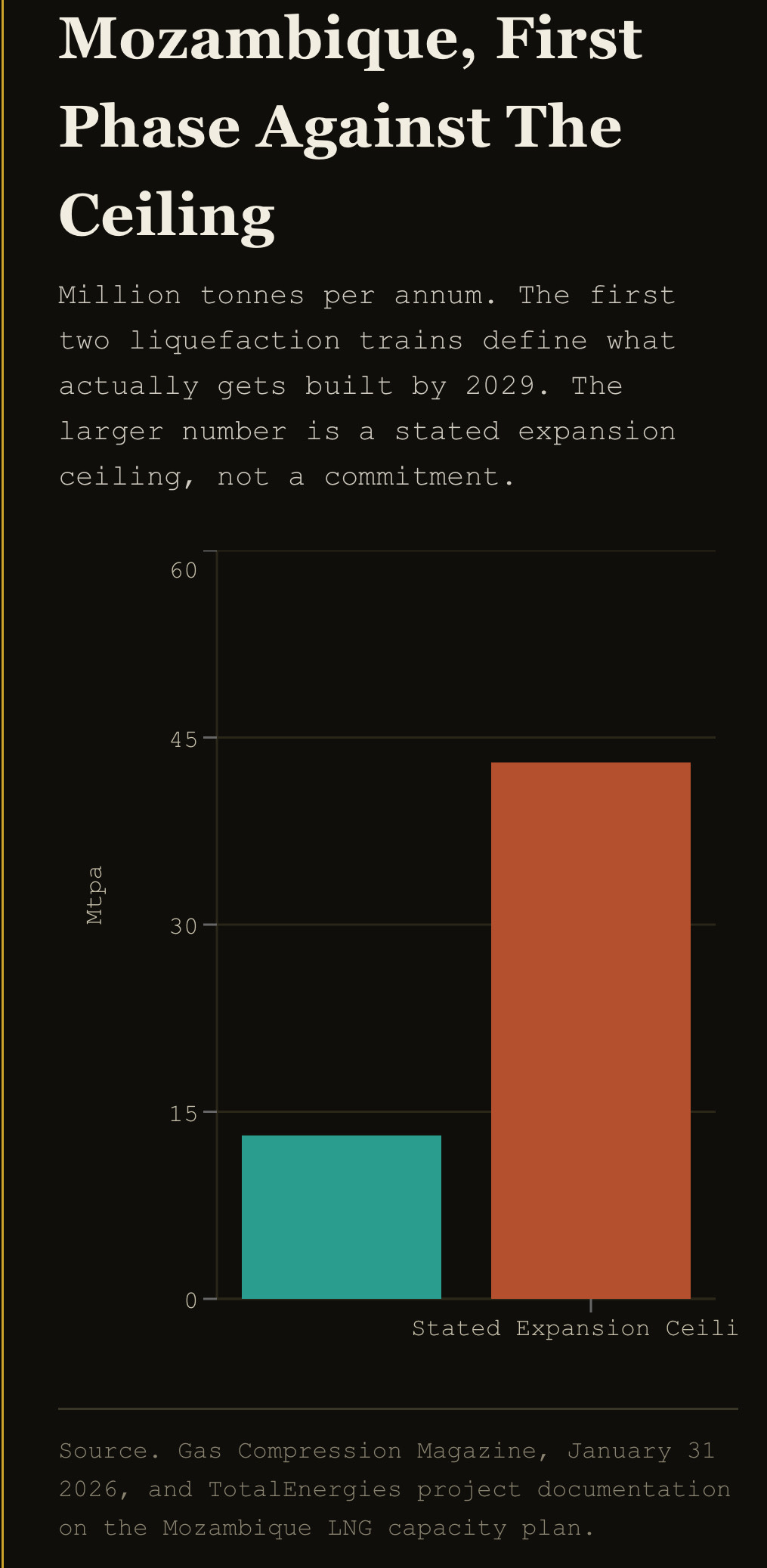

Run that logic through TotalEnergies’ own numbers and the LNG pillar becomes the thing to watch. Mozambique LNG is designed to begin at thirteen point one million tonnes a year across its first two liquefaction trains, with a stated expansion ceiling reaching as high as forty three million tonnes if later phases go ahead, and that eventual capacity lands in the same ocean as Qatar’s North Field expansion, the American Gulf coast build out including TotalEnergies’ own Rio Grande project, and a dozen smaller projects racing toward first cargo by the end of the decade. China exports deflation into every manufacturing category it decides to scale, and gas is no different once enough liquefaction capacity floods a market simultaneously. TotalEnergies spent 2025 proving its four pillar structure can absorb an eleven dollar drop in oil. The real test arrives when LNG prices take the same kind of hit oil just did, at the exact moment Mozambique’s first phase, Qatar, and the American Gulf coast all reach meaningful capacity within the same eighteen month window.

STRESS TEST

Mozambique carries the largest single project risk on the balance sheet. Fifteen billion dollars in remaining capital sits inside a province where the underlying insurgency has not disappeared, only receded, and where two open French legal proceedings could still surface documents that complicate the very restart the company just celebrated.

Uganda carries reputational and eventually financial risk rather than operational risk, since EACOP is already under construction regardless of what a Paris court decides. A reparations ruling against TotalEnergies would not stop the pipeline, but it would set the first substantive precedent under France’s duty of vigilance law, inviting the same theory against every other French multinational operating in a fragile state.

The American wind buyback is politically costless today and could become expensive tomorrow. If the blue state lawsuit succeeds in unwinding the settlement, TotalEnergies could face a clawback fight over money already redeployed into Rio Grande LNG, precisely the kind of headline risk a company otherwise trying to look like a reliable American energy investor cannot afford.

LNG oversupply is the variable TotalEnergies cannot negotiate its way around with any government. Four pillars diversify commodity exposure within oil and gas and power, but Integrated LNG and the American gas buildout it just accelerated with taxpayer money both sit on the same side of a coming supply wave.

THE INSTITUTIONAL LABEL

TotalEnergies integrates. Not just barrels and molecules and electrons under one balance sheet, but governments too, treating Washington, Paris, Maputo, and Kampala as four more inputs to be balanced against each other rather than four separate relationships to manage in isolation. Burgum hands it a check to stop building wind. Chapo hands it security cover to restart gas. Le Maire once threatened a fight it never had to finish. A Paris judge keeps ordering it to hand over documents it would rather keep. TotalEnergies absorbs all four inputs the same way it absorbed an eleven dollar drop in Brent, and the company that comes out the other side rarely looks like it flinched.

SOURCES

TotalEnergies fourth quarter and full year 2025 results press release and results presentation, February 11 2026. Businesswire, Hellenic Shipping News, Enerdata, and StockTitan coverage of the same results, February 2026. StockTitan Form 20-F and Form 6-K filings, TotalEnergies SE, February and March 2026. US Department of the Interior press release, March 23 2026, offshore wind lease settlement. CNN, ABC News, PBS News, Heatmap News, Canary Media, and Kavout Market Lens, coverage of the TotalEnergies wind buyback and the seven state lawsuit, March through June 2026. Gas Compression Magazine, Rio Times, Al Jazeera, Offshore Energy, Natural Gas Intelligence, and TotalEnergies press releases, Mozambique LNG restart, January 2026. Business and Human Rights Resource Centre, Les Amis de la Terre, Survie, Novethic, Decideurs Juridiques, and Energy Voice, EACOP and Tilenga duty of vigilance litigation, 2021 through September 2025. Energynews.pro, Reuters via Yahoo Finance, Juristique, and TotalEnergies investor relations FAQ, ADR to ordinary share conversion and New York listing history, 2024 through 2026. Euronews, May 2 2024, Bruno Le Maire remarks on a full New York relocation. CNBC, Amrita Sen interview, June 29 2026. CNBC via Yahoo Finance, Kevin Hassett interview, June 2026.